In the face of mounting debts, many middle-class families in 2023 are finding themselves in financial quicksand. As the ground beneath their feet sinks with each passing day, they might feel that escape is impossible. But hold tight, folks, because we’re about to throw you a rope! You’ll still have to catch it though. We’ve dived deep into the data to bring you this guide. By honing specific financial habits, you can not only manage your debt but potentially eliminate it altogether for your family.

In this guide, we’ll dive into the key financial habits that can help you regain control over your debts and pave the way to financial freedom for your family. From setting realistic goals to creating a budget, from prioritizing debt repayment to building an emergency fund, we’ll provide practical strategies and tips to get you on the path to a debt-free future.

So, if you’re ready to break free from the grip of debt and take charge of your financial well-being, keep reading. We’re here to equip you with the knowledge and tools you need to turn your family’s financial situation around and thrive in 2023 and beyond.

What is Debt?

Picture debt like a sort of financial flu. Have you ever found yourself in a situation where you owe more money than you actually have? It could be a mortgage for that dream home you cherish, a student loan that supported your education, a personal loan that got you through a difficult period, or even credit card debts from unexpected car repairs or spontaneous vacations. But unlike the common flu, debt doesn’t magically disappear with a spoonful of grandma’s chicken soup. It requires a powerful combination of strategic planning and effective financial habits that YOU have to build!

What are Financial Habits?

Now, imagine financial habits as the ingredients in that potent and healing mix of broth. These are repeated behaviours that have a significant impact on your financial health. Just like how maintaining good oral hygiene by brushing your teeth daily keeps your smile bright and healthy, adopting effective financial habits ensures that your money matters remain in top shape. These habits may include creating a budget, consistently saving a portion of your income, or prioritizing your needs over your wants. However, it’s important to remember that not all financial habits will work for everyone, just as not all ingredients are suitable for every dish. It’s about finding and cultivating the habits that work best for your personal family situation.

Decoding Debt Management: 2023 Insights

In the depths of debt, there’s a light at the end of the tunnel. Acknowledging your debt is the first step toward financial stability. Despite the growing Canadian household debt, the insights drawn from two recent comprehensive analyses by CMHC and Statistics Canada show that there are ways to balance your books and start your journey to financial stability for your family.

CMHC’s Insights

Quick Facts:

- Canada holds the highest level of household debt among G7 countries.

- Mortgages make up three-quarters of this debt.

- Household debt has risen steadily over the years, exceeding the economy’s size in 2021.

- The Bank of Canada’s increased interest rates to combat inflation have resulted in higher mortgage payments.

The CMHC report depicts a clear picture of Canada’s significant household debt, comparable to a towering redwood in a forest of pines. Much like a precarious Jenga tower, this economic situation leaves Canada susceptible to global downturns. A fancy way to say “there might be dangers ahead”. The consequences of such high household debt can be catastrophic, akin to a large, lurking iceberg on our economic horizon. But the report suggests potential strategies to mitigate the crisis, like increasing the housing supply and rejuvenating Canada’s rental stock, to reduce the pressure on Canadians to become homeowners. Translation, actually help Canadians pay reasonable rent vs our current landscape.

Statistics Canada’s Insights

Quick Facts:

- Despite a decline in the household saving rate in Q1 2023, the household sector net worth rose $519.9 billion.

- The pace of credit market borrowing has decelerated. (Say hello to high interest rates)

- Household credit market debt as a proportion of household disposable income has increased to 184.5%.

- The household debt service ratio has risen to 14.90% in Q1 2023.

The Statistics Canada report shines a light on the flip side of the coin. Even as the household saving rate has dipped, the household sector net worth rose significantly, indicating strength in the equity and real estate markets. Additionally, the pace of borrowing has slowed, showing a more cautious approach to debt. However, the increase in household credit market debt relative to disposable income suggests increased financial stress among households. Don’t forget, even though the real estate market is holding up, it doesn’t mean that things are cracking underneath. We currently do not have enough homes to house our growing population, therefore, since there is an unusually high demand, prices will remain high for the foreseeable future unless a drastic event happens. This is the tough game the Canadian housing market and the Government of Canada is playing.

The landscape of debt management may seem daunting, like a hiker lost in the wilderness. However, armed with the right tools and strategies drawn from these insights, it’s possible to navigate the way to financial stability. The key is to see these challenges not as insurmountable obstacles, but as opportunities to cultivate sound financial habits or at the very least opportunities for learning to grow your own knowledge. With these in mind, we can march forward, overcoming each debt hurdle, and move towards a future filled with financial possibilities.

Understanding Your Debt Spectrum

Debt isn’t always a four-letter word. Used wisely, it can be a powerful tool, fueling our economic engines, and opening the doors to opportunities, from owning a home to launching a business. It’s all about understanding and strategically managing your debt spectrum. At some point down the road, your financial education will take you places such as learning to use other people and their money to buy things vs your own, welcome to the art of leverage (keep reading to learn more!).

Types of Debt

Quick Facts:

- Consumer Debt: Credit cards, personal loans (like student debt), or auto loans can provide the flexibility to manage cash flow and make significant purchases. Meaning you get to borrow money to buy things now and pay for them later.

- Mortgage Debt: A route to home ownership, often with tax benefits and historically low-interest rates. (I know, I know, this isn’t quite true at the moment… but we had a good run for the last few years)

- Medical Debt: Ensuring healthcare needs are met, often due to unforeseen circumstances. Emergencies not covered by our healthcare.

Understanding your debt spectrum is the first step toward making it work for you. Consumer debt, though typically carrying higher interest rates, can provide much-needed liquidity in times of need. But you’ll generally want to prioritize this category first. Mortgage debt, often the most substantial part of a majority of a family’s debt profile, offers the advantage of historically low-interest rates and potential tax deductions. Investments in oneself, like student debt, can open doors to higher earning potential, and medical debt, albeit often unplanned, ensures our most crucial asset – our health.

Debt Management Strategies

Quick Facts:

- Debt Consolidation: Streamline multiple debts into a single one, potentially reducing your interest rate and simplifying management. Be cautious because it doesn’t affect your credit history, so use it as a last resort.

- Debt Settlement: Negotiate with creditors to reduce the overall debt owed. While “settlement” sounds final, you can also call them up regularly as long as you have been paying your bills and negotiate with them to try and lower your interest rate. Remember, the interest you pay is what makes the company money, so even though you’re in debt, you still have leverage and can negotiate so go for it!

- Refinancing: Replace an existing debt obligation with another under different terms, often to secure a lower interest rate or to leverage equity.

- Debt Snowball or Avalanche Methods: Strategies to pay off individual debts in order to minimize interest payments or to gain momentum in your debt reduction journey. Usually achieved by only focusing on ONE debt item at a time, the one with the highest interest rate.

Each debt management strategy comes with its own set of benefits. Consolidating your debt can make your debt landscape easier to navigate, with one monthly payment and potentially a lower interest rate. Would be great if you’re someone who’s often forgetful and misses payments. Debt settlement can reduce the overall mountain of debt that you’re chipping away at, while refinancing can take advantage of shifts in the economy to make your debt work better for you. Finally, the snowball or avalanche methods can build momentum of their own, rolling towards a debt-free future. Really great for building good habits!

Armed with this understanding, you can turn your debts from threats into opportunities, turning the tables on your financial challenges and leveraging your debts into strategic assets. Because, after all, a well-managed debt is not a burden, but a bridge to achieving your financial goals. Remember, you do not have to tackle these all at once, pick one that you feel comfortable with and start there. Consistency is what wins the game in the end, your gusto of doing everything all at once might fail or cause burnout. Take your time, slow and steady.

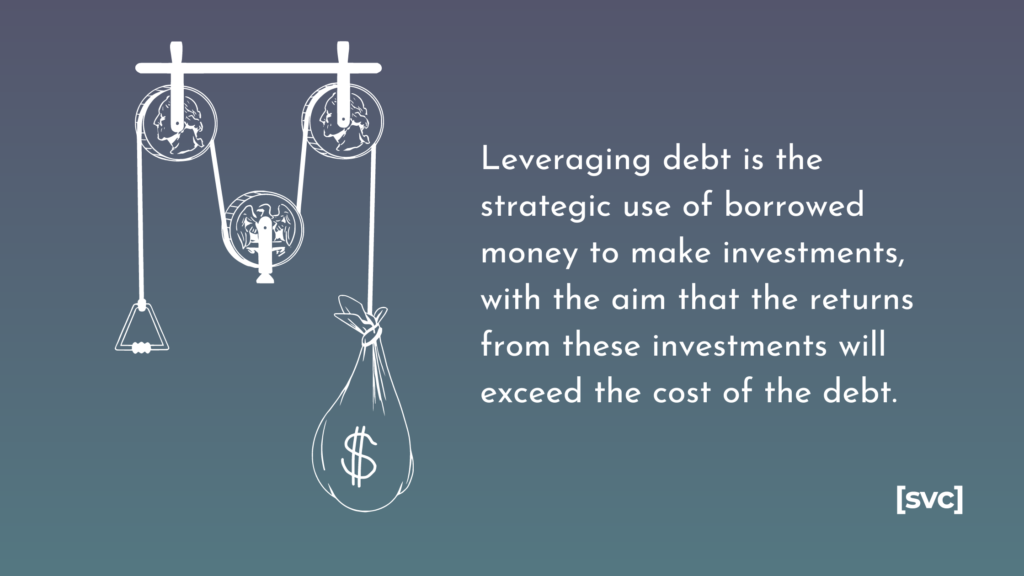

Leveraging Debt: The Flip Side of the Coin

Debt, often viewed as a hurdle to financial freedom, can in fact be a stepping stone when strategically used. The key lies in understanding how to leverage it. Leveraging debt refers to the practice of using borrowed money for an investment with the hope that the profits from the investment will exceed the cost of the debt.

Quick Facts:

- Mortgage Debt: Can be leveraged to own a home that can appreciate over time, yielding a profit when sold. Or using the existing capital to make a new purchase.

- Business Loans: Used to expand operations, buy equipment or even launch a business, with the aim that the business’s returns will surpass the loan’s costs.

- Low-Interest Loans: Can be leveraged to invest in high-return opportunities, effectively profiting from the interest rate differential. Or even to reduce your consumer loan interest like paying off a credit card.

- Credit Cards: Points, cashback, or other rewards can be leveraged for savings if the balance is paid in full each month. EVEN if you carry a balance, don’t skimp out on that $50 – $100 grocery cash reward you might get just by using your credit card!

Mortgage debt can be a classic example of leveraging debt. Buying a house with a mortgage allows you to own and live in a house that might appreciate in value over time. When you sell, the profit could exceed the cost of your mortgage debt, effectively making your debt a profitable investment. That’s the basics, experienced real estate investors would leverage the cash flow of their existing property to get a leg up in purchasing their second real estate property and making the first one a rental.

Business loans are another way to leverage debt. Used to grow the business faster, say you make t-shirts and you’re confident you can sell 500 but you only have the money to purchase 100 to keep as inventory. You get a loan so you can quickly get 500 t-shirts and then sell at a profit, therefore paying off your loan with your new profits.

Low-interest loans, such as student loans or home equity lines of credit, can be leveraged by investing the borrowed funds into higher-return opportunities. This strategy banks on the return on investment (ROI) being greater than the loan’s interest rate. Not quite the case anymore for student loans but we can still learn from the concept.

Credit cards, though typically associated with high-interest rates, offer a chance to leverage debt in the form of rewards. If you pay your balance in full each month, you can take advantage of points, cashback, or other rewards without paying interest. It is LEGIT getting free money if you can’t wrap your mind around this. DM me for a free call, and let’s chat about that wealth mindset.

Remember, leveraging debt involves risks. It should be approached with a solid understanding of your financial situation and tolerance for risk. The potential for greater returns often comes with increased risk, so it’s crucial to make informed decisions. When utilized wisely, leveraging can serve as an accelerant to your financial goals, propelling you towards your financial future. If you’re not ready, there’s no shame in that. Start with practicing your habits first, leveraging is like level 5 of your financial game. It’s here to inspire you to get to this level, not jump into the deep end and drown.

Blueprint to Break the Debt Chains

With data as your compass and financial acumen as your weapon, breaking free from the shackles of debt can be more than just a far-off dream. It’s a journey made up of small, practical steps, taken consistently over time. No get rich quick schemes. Here, we outline proven strategies that you can incorporate into your daily routine to pave your way to financial freedom.

1. Track Your Expenses

Start by understanding where your money goes. Use apps or good old-fashioned spreadsheets to record every dollar spent. This activity serves as the bedrock of sound financial management by revealing your spending habits, pinpointing unnecessary expenses, and shedding light on potential areas of savings. I had used the notes section on my phone and still keep an Evernote file, no joke – it works for me.

2. Create a Realistic Budget

Building on your expense tracking, devise a budget that reflects your financial reality. Align your budget with your income, mandatory expenses like bills, loan repayments, and essential needs. Remember to include contributions to savings and discretionary spending. The key is to create a budget that is achievable, flexible, and accounts for occasional indulgences. If you can’t save anymore right now, that is TOTALLY FINE! Create a line item for future savings when your income increases and fill it in when you have extra money. Don’t get discouraged and write it off. While it’s great to have money for savings, our family has legit made over 10K/month and was unable to put aside savings/investments.

3. Prioritize Your Debts

All debts are not created equal. Some may bear heavy interest rates or penalties or a mental load! Prioritize your debts, focusing on paying off high-interest ones first (a strategy known as debt avalanche), or tackling smaller debts for quick wins and motivational boosts (known as debt snowball). The method you choose largely depends on your personal preferences and financial circumstances. There is no right or wrong answer here, do what feels most comfortable for your family or what will bring you peace of mind. I chose to pay off my student loans over credit card debt because it was such an eyesore – never regretted my decision even though we paid a few extra hundred in credit card interest. You truly cannot put a price on peace of mind, money is sometimes emotional, and not all decisions have to be logical.

4. Leverage Your Assets

Assets—like your home, investments, or even your skills—can serve as powerful tools to mitigate debt. Consider renting out a portion of your house, selling unused items, investing wisely, or monetizing your talents to generate additional income. Remember, wealth isn’t just about the money you save—it’s also about the assets you wisely utilize.

5. Build Emergency Savings

As you work your way out of debt, don’t forget to cushion yourself against unexpected financial shocks. Aim to save three to six months’ worth of living expenses. Start small if necessary, and remember, a little is better than nothing. Having emergency savings reduces the need to rely on debt in unexpected situations. When I say start small, even if you start with $1 it’s better than nothing. Why? Because you’re building a habit and not aiming for perfection! Of course, it’ll take forever if you ONLY contribute $1 a month BUT, if you get into the habit of setting aside money for an emergency fund, you’ll eventually want to increase it because you see it EVERY MONTH. Consistent practice is what wins the game, not your momentary spurts. If you have a job that gives you bonuses, this would be a great time to contribute more to your emergency fund if you’re usually tight in your monthly budget.

6. Regularly Monitor Your Progress

Just like a regular health check-up, a periodic financial review is essential. Adjust your budget as required, celebrate your wins (big or small), learn from your missteps, and stay motivated. Seeing your debt decrease over time can provide the necessary momentum to keep going. No shame, I low-key do this still, every week . Not because I have to but simply because I want to. I want to be able to adapt faster to our spending, to discover trends, but that is me. I love managing our finances and it gives me joy. But if you hate it, start small, quarterly check-ins are just fine. Money is personal, you create a system that works for you.

7. Seek Professional Help

Don’t hesitate to seek help from financial advisors or credit counselling agencies, especially when dealing with substantial debt. They can provide personalized strategies, negotiation assistance with creditors, and resources to manage and reduce your debt effectively. Remember, asking for help isn’t a sign of weakness—it’s a step toward empowerment. Or you know, wealth coaches like me. Sometimes we just need a cheerleader in our corner to help keep us on track. Remember, you do not have to do this alone. Help exists out there!

Your debt doesn’t define you. With determination, discipline, and the right strategies, you can break the chains of debt and take control of your financial future. Believe in your power to change your financial reality. After all, the journey of a thousand miles begins with a single step. I know, cheesy, but I’m trying to be supportive here, okay?

Making Financial Habits Stick

Developing a new habit is one thing; maintaining it is another. We’ll delve into strategies that can help ensure these effective financial habits become part of your daily routine. After all, it’s persistence that turns a new behaviour into a long-lasting habit.

1. Start Small

Begin with manageable goals. Instead of aiming to save half your income right away, start by saving a small percentage and gradually increase it. Small wins will motivate you to continue and make the process less overwhelming. Still too much? Learn one financial habit, before starting to practice, do your research and see which financial habit you’d like to first learn. THEN start your practice.

2. Be Consistent

Consistency is key in habit formation. Make sure to stick to your new financial practices daily. Whether it’s updating your expense tracker, reviewing your budget, or setting aside savings, consistency will engrave these habits into your routine. Note, it’s also okay to take breaks. If you can’t do it daily, do it week, monthly, or whatever timeframe you choose to be consistent. And know it’s okay to take breaks. If you start daily and you realize it’s too overwhelming, scale it back to weekly. Don’t put so much pressure on yourself, consistent isn’t something you can master in a day or even a month. But with enough time and dedication, it’ll become something that you won’t even have to think about.

3. Use Tools and Reminders

Leverage technology to your advantage. Use budgeting apps, expense trackers, and automated reminders to keep you on track. These tools can help you monitor your financial habits and ensure you don’t overlook important tasks. If these overwhelm you, a good old journal/notebook like this one will do the trick too. Don’t let excuses get in the way!

4. Make It Enjoyable

Find ways to make the process enjoyable. Perhaps you love visualizing progress—then, use colourful charts to track your debt reduction. Or if you’re a social person, join a money management group or forum. When you enjoy what you’re doing, you’re more likely to stick to it.

5. Reward Yourself

Rewards are a powerful motivator. Treat yourself (within your budget, of course!) whenever you hit a financial goal. This could be paying off a certain amount of debt, saving a specific sum, or even consistently tracking your expenses for a month. A treat doesn’t have to cost money, it would be simply sleeping in, or having a second slice of cake.

6. Stay Educated

Stay informed about personal finance. Regularly read books, and articles, or listen to podcasts on the subject. The more you learn, the more equipped you’ll be to make sound financial decisions and keep up your good financial habits. To win the game of personal finance is not a one-and-done game. This is why I say start small, it’s forming a lifelong habit.

7. Be Patient

Rome wasn’t built in a day, and neither is financial independence. It takes time to see significant changes, and that’s okay. Be patient with yourself, and remember that each step, no matter how small, brings you closer to your financial goals.

Building strong financial habits might seem challenging (and it IS!), but with persistence and the right strategies, it’s completely achievable. And the rewards — financial stability, peace of mind, and freedom from the chains of debt — are absolutely worth it. Remember, the power to change your financial future is in your hands, and the journey starts with the habits you cultivate today.

Building Strong Financial Habits

Debt doesn’t have to be a life sentence. With the right financial habits, strategies, and a hefty dose of perseverance, middle-class families can crush their debts and emerge with robust financial health. From understanding your debt spectrum to leveraging debt wisely, creating a realistic budget to tracking expenses, every financial habit you adopt brings you one step closer to financial freedom.

In the face of the challenging debt landscape of 2023, armed with these data-driven strategies, you’re no longer standing on sinking sand. You’re standing on a ladder, each rung a financial habit bringing you higher above the debt abyss. Start climbing today and create a financial future where you’re in control, not your debts.

Because, after all, financial freedom is not just about the destination. It’s about the journey. It’s about transforming your financial habits, evolving your mindset, and empowering yourself and your family to carve your path through the debt wilderness. You’ve got the roadmap. Now, all you need to do is start walking.